A Simple Way to Invest

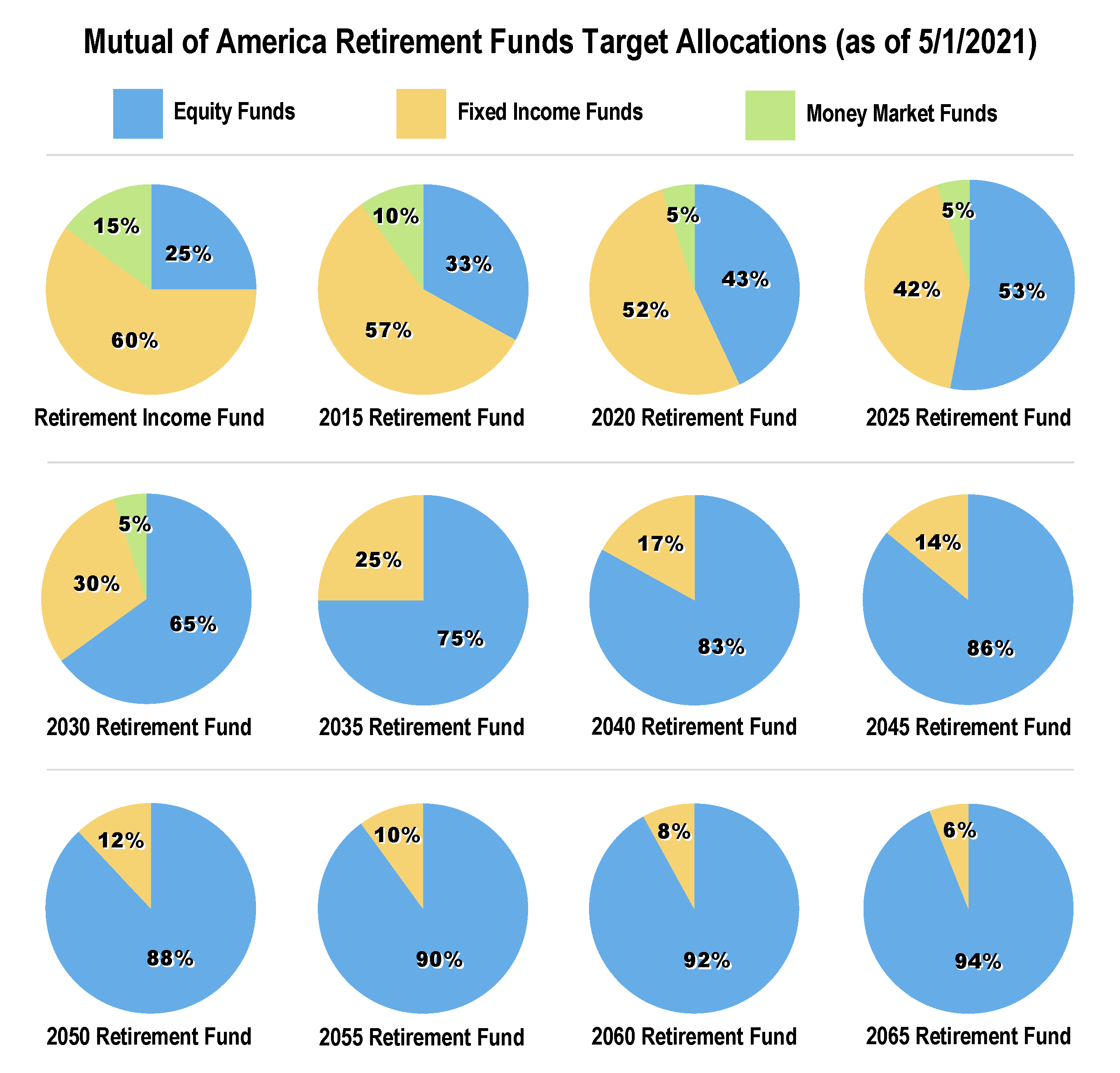

Mutual of America Investment Corporation Retirement Funds provide a simple retirement strategy. They offer the advantage of a diversified "fund of funds" approach within a single Fund, with the added benefit of professional asset allocation (the mix of stocks, bonds and money market funds). Each Retirement Fund will invest in certain other Mutual of America Investment Corporation Funds.

Put another way, the Retirement Funds are designed to offer investors a plan that simplifies the asset allocation decision prior to and continuing into retirement.

Is a Retirement Fund right for you? Asset Allocation Made Easier

The Retirement Funds that are geared to an estimated retirement date have an asset allocation mix among equities (stocks), fixed income (bonds) and short-term investments that is designed to be more aggressive for individuals with a larger time horizon to retirement, and become more conservative as you near retirement.

The Retirement Income Fund

The Retirement Income Fund is intended for investors who have reached retirement or have passed their anticipated retirement year, and seeks current income consistent with preservation of income and, to a lesser extent, capital appreciation.

The Retirement Income Fund is comprised of a mix of primarily fixed income funds, equity funds and a money market fund.

When the Retirement Year Is Reached

Many investors can expect to live for a significant time period after retirement. Although capital preservation becomes a primary consideration during retirement, growth is also an important consideration to help offset the negative impact of inflation.

As a result, a year-specific Retirement Fund that has reached its target retirement date may have as much as 45% of its assets invested in equities.

Such a maturing Retirement Fund will move toward the allocation mix of the Retirement Income Fund over the 10-year period after the retirement year has been attained.

At any time within 10 years after a Retirement Fund has reached its target retirement year, the assets may be transferred into the Retirement Income Fund if approved by the Board of Directors of Mutual of America Investment Corporation. The maturing Retirement Fund will then cease to exist, and its participants will automatically become participants in the Retirement Income Fund.

The value of a Retirement Fund is not guaranteed at any time, including at and after the target date. There is no guarantee that a Retirement Fund will correctly predict market or economic conditions, and as with other mutual fund investments, you could lose money. In addition to a retirement date, individuals should consider their risk tolerance, time horizon, personal circumstances and complete financial situation before investing.

You should consider the investment objectives, risks, and charges and expenses of the variable annuity contract and the underlying investment funds carefully before investing.

This and other information is contained in the contract prospectus or brochure and underlying funds prospectuses and summary prospectuses,

which can be obtained by calling 800.468.3785 or visiting mutualofamerica.com. Read them carefully before investing.

Mutual of America's group and individual retirement products are variable annuity contracts and are suitable for long-term investing, particularly for retirement savings. The value of a variable annuity contract will fluctuate depending on the performance of the Separate Account investment funds you choose. Upon redemption, you could receive more or less than the principal amount invested. A variable annuity contract provides no additional tax-deferred treatment of benefits beyond the treatment provided to any qualified retirement plan or IRA by applicable tax law. You should carefully consider a variable annuity contract's other features before making a decision.